Budget Questions Answered: Negative Gearing, New Builds & Trusts

- May 16

- 2 min read

Following the federal budget announcement, many Australians were left with one big question:

“What exactly changes now?”

Below is a simplified breakdown of some of the most common questions raised after the budget — especially around negative gearing, CGT, housing supply and trusts.

1. What actually counts as a “new build” under the new negative gearing rules?

The key principle is simple:

The government only wants to preserve negative gearing benefits for properties that add to Australia’s housing supply.

That generally includes:

Brand new houses

New apartments

Newly constructed townhouses

Subdivision projects creating additional dwellings

If you are the first owner of a newly completed property, it will generally qualify.

But if someone else already bought it before you — even if only six months ago — it likely no longer counts as a new build for the tax concessions.

2. What if I knock down an old house and rebuild?

This is where it gets more specific.

Scenario 1:

You knock down one house and rebuild one house.

That does not count as adding supply.

Result:No access to the new negative gearing treatment.

Scenario 2:

You knock down one house and build two dwellings.

That does add supply.

Result:Both properties may qualify.

This distinction is likely to become extremely important for developers, builders and small-scale investors.

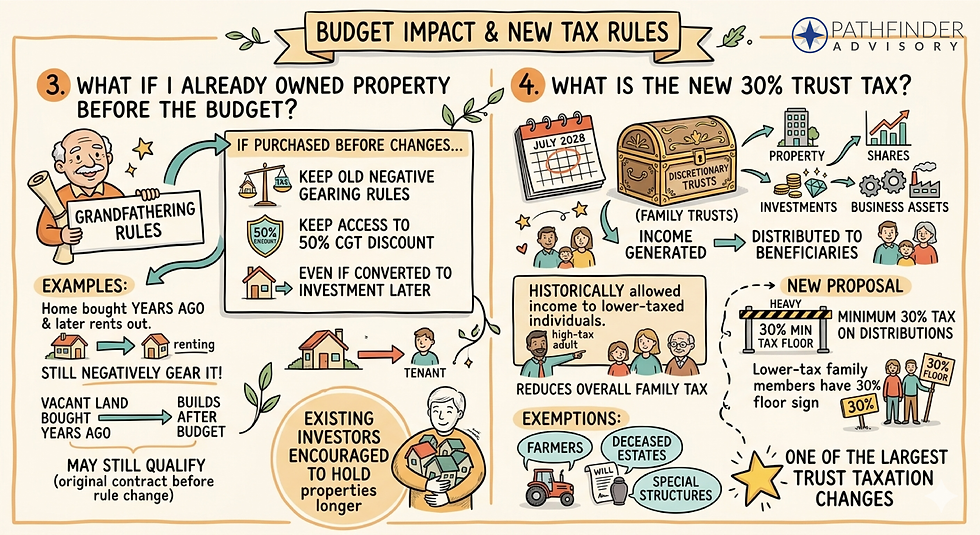

3. What if I already owned the property before the budget?

This is where grandfathering comes in.

If you purchased the property before the changes took effect:

You keep the old negative gearing rules

You keep access to the 50% CGT discount

Even if you later convert the property into an investment

For example:

Someone who bought a home years ago and later rents it out can still negatively gear it.

Someone who bought vacant land years ago and builds after the budget may still qualify because the original contract was entered into before the rule change.

This is why many existing investors may now be encouraged to hold properties longer rather than sell.

4. What is the new 30% trust tax?

One of the lesser-discussed budget measures was the proposed minimum 30% tax on discretionary trusts.

These changes are expected to begin from July 2028.

Discretionary trusts — often called family trusts — are commonly used to hold:

Property

Shares

Investments

Business assets

The income generated can then be distributed among beneficiaries.

Historically, this allowed families to distribute income to lower-taxed individuals, reducing the overall family tax burden.

For example:

Someone earning at the highest marginal tax rate may distribute trust income to adult children or lower-income family members who pay less tax.

The new proposal effectively introduces a minimum 30% tax floor on those distributions.

There are expected to be exemptions for:

Farmers

Deceased estates

Some other special structures

But overall, this represents one of the largest trust taxation changes seen in many years.

*This is not a financial advice. Information is for general purpose only.